You can start Social Security at 62. Almost nothing else about the decision is that simple — and the cost of getting it wrong compounds for the rest of your life, because claiming early is not a temporary discount. It is permanent.

The Social Security Administration publishes all of this, in plain language, across three pages most people never open. Here is what they say.

Checkpoints

- Earliest claim is 62, with a permanent reduction for every month before your full retirement age

- Full retirement age is 67 for anyone born in 1960 or later

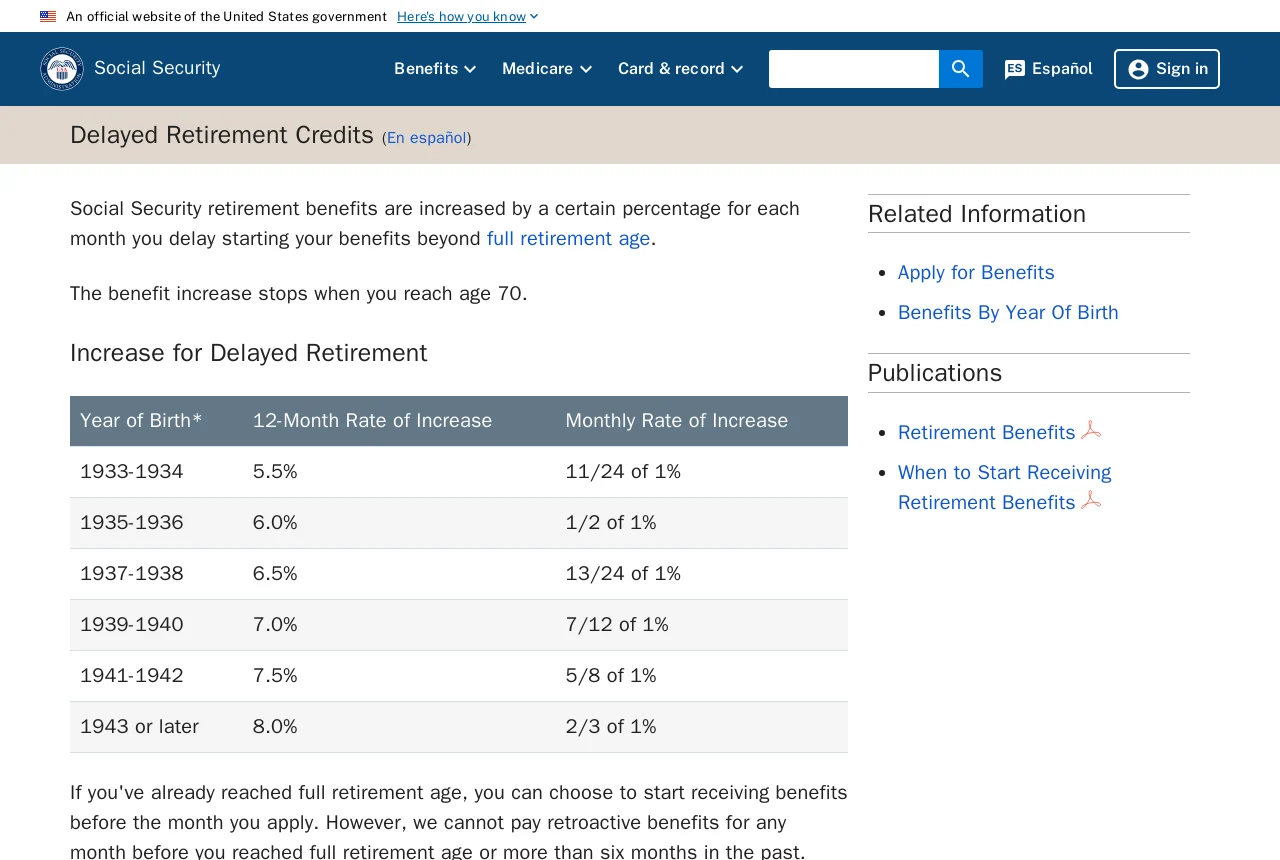

- Delaying past full retirement age adds 8% a year — and stops at 70

- Sign up for Medicare at 65 even if you are delaying Social Security

1 Open a my Social Security account and read your own statement

Create the account at ssa.gov/myaccount. It is free, and it lets you estimate future benefits, check an application’s status, request a replacement card, and manage benefits you already receive.

Signing up requires a Login.gov or ID.me credential. SSA says there is no wrong choice between them.

Inside, read your Social Security Statement. The estimates there are computed from your own earnings history, which is the only version of this decision that matters. If your earnings record has a gap or an error, this is where you find it — and you want to find it decades before you claim.

2 Understand what early and late actually cost

Your full retirement age depends on your birth year. For everyone born in 1960 or later it is 67. That is the age at which you receive 100% of your benefit.

Claim before then — as early as 62 — and SSA reduces your benefit by a small percentage for each month you claim early. The reduction does not reverse when you reach full retirement age. It is the amount you receive for life.

Delay past full retirement age and you earn delayed retirement credits. For anyone born in 1943 or later, that is an 8% increase for each year you wait. Crucially, the credits stop at 70. Waiting past your seventieth birthday adds nothing at all — it simply forfeits the checks you could have collected.

3 If you keep working, learn the earnings test

Collecting benefits before full retirement age while still working triggers the retirement earnings test. If you are under full retirement age for the whole year and earn above the annual limit, SSA withholds $1 for every $2 above it.

In the calendar year you actually reach full retirement age, the rule loosens: SSA withholds $1 for every $3 above a higher limit, and counts only what you earn before the month you hit that age. From the month you reach full retirement age onward, there is no limit at all — earn whatever you like.

Here is the part almost everyone misses: the withheld money is not gone. When you reach full retirement age, SSA recalculates your benefit to credit the months in which payments were reduced. The earnings test defers benefits; it does not confiscate them.

The annual limits themselves change every year, so read them on SSA’s own page rather than from an article.

4 Common mistakes, and how to avoid them

Mistake 1

Treating a benefit claimed at 62 as “full.” It is a permanent reduction that never resets.

Mistake 2

Delaying past 70 in the belief that the benefit keeps growing. Delayed retirement credits stop at 70.

Mistake 3

Believing the earnings test destroys benefits. Withheld amounts are recredited at full retirement age.

Do this today

Create your my Social Security account and read the estimate built from your own earnings record. Check the record itself for missing years while there is still time to fix it.

FAQ Frequently asked questions

What is the earliest I can claim, and what does it cost?

Age 62. Benefits are permanently reduced by a small percentage for each month you claim before your full retirement age. Waiting until full retirement age gives you the full amount, and delaying beyond it increases the benefit until age 70.

What is full retirement age?

The age at which you receive 100% of your benefit. It depends on your birth year; for people born in 1960 or later it is 67, according to SSA’s chart.

Can I work while collecting Social Security?

Yes. Before full retirement age, earnings above an annual limit reduce your benefit by $1 for every $2 over it, or $1 for every $3 in the year you reach full retirement age. From the month you reach that age there is no limit, and the withheld amounts are recredited to you.

Key takeaways

- Claiming at 62 permanently reduces your benefit; 67 is full retirement age for those born 1960+

- Delayed retirement credits add 8% per year and stop dead at 70

- The earnings test defers benefits, it does not take them — and it ends at full retirement age

- Enroll in Medicare at 65 even if you delay Social Security